EOFY, Performance Data and Property Investing in 2026: Tax Time Tips for Australian Investors

As June 30 approaches, Australian property investors are once again turning their attention to end of financial year planning. For many investors, tax time is viewed as a compliance task. In reality, it is also a valuable opportunity to review cash flow, check loan structures, assess portfolio performance and prepare for the next stage of your investment journey.

In 2026, EOFY has added importance. The ATO has released updated rental property guidance, rental deductions remain a key compliance focus, and the Federal Government has announced proposed changes to negative gearing and capital gains tax from 1 July 2027. These changes are not yet law, but they are important enough for investors to understand and factor into their FY27 planning.

At Sound Property, we believe tax time should never be treated in isolation. A strong tax position is useful, but it should support a broader investment strategy built around asset selection, cash flow, risk management and long-term capital growth.

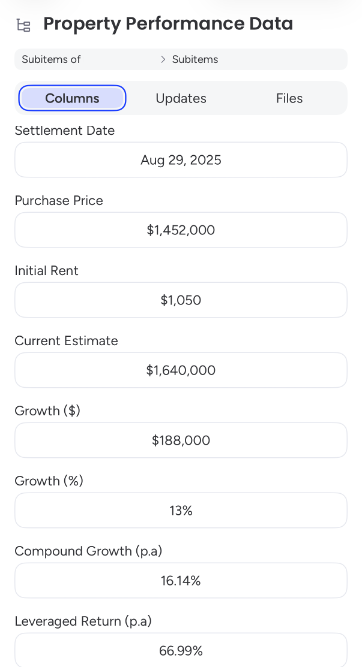

As part of our ongoing commitment to supporting clients beyond settlement, we’ve been working on a number of improvements behind the scenes and are pleased to let you know that we’re rolling out a new feature on our Client Portals.

Your Client Portal will serve as a central location for your property information and ongoing performance tracking. The new Property Performance Data within the Client Portal will allow you to track:

Property Performance Data

|  |

Why EOFY matters for property investors

EOFY is your annual checkpoint. It is a chance to make sure you are claiming what you are entitled to, keeping the right records and making informed decisions about your portfolio.

For residential property investors, common deductible expenses may include loan interest, property management fees, council rates, water charges, strata levies, insurance, repairs, maintenance and depreciation. The key is making sure each expense is correctly classified and supported by evidence. The ATO’s 2026 rental property guide continues to separate expenses into broad categories: costs that may be claimed immediately, costs that are claimed over time, and costs that are not deductible.

Get your paperwork organised early

Good records are the foundation of a smooth tax return. Before speaking to your accountant, gather your loan statements, rental statements, property management invoices, council and water rates, strata notices, insurance documents, repair invoices, depreciation schedule and purchase or sale documents if you transacted during the year.

This is especially important if your investment loan has been refinanced, redrawn or mixed with private spending. The ATO is clear that interest is only deductible to the extent the borrowed funds are used for income-producing purposes. If part of the loan has been used for personal expenses, the interest may need to be apportioned.

SP insight: Do not rely on bank summaries alone. Keep a clean file for each property so your accountant can quickly identify income, expenses and any items needing special treatment.

Review repairs, maintenance and improvements

One of the most common tax-time mistakes is confusing repairs with improvements.

A repair generally restores something to its previous condition, such as fixing a leaking tap, replacing broken tiles or repairing storm damage. These costs may often be claimed immediately if they relate to wear and tear while the property was rented or genuinely available for rent.

An improvement usually makes the property better than it was before, such as a new kitchen, bathroom renovation, extension or major upgrade. These costs are usually capital in nature and claimed over time rather than immediately. The ATO’s updated rental guidance continues to place strong emphasis on getting this distinction right.

SP insight: If you are planning upgrades before June 30, speak with your accountant first. The timing, reason and nature of the work can affect how the expense is treated.

Check your depreciation position

Depreciation can make a meaningful difference to after-tax cash flow, particularly for newer properties or properties with eligible plant and equipment.

In simple terms, depreciation allows investors to claim the decline in value of certain assets, or the construction cost of the building, over time. Some lower-cost depreciating assets may be claimed immediately if they meet the ATO’s rules, including assets costing $300 or less used for a taxable purpose.

SP insight: If you purchased an investment property during FY26 and have not ordered a depreciation schedule, this should be on your EOFY checklist. Even some older properties can have claimable capital works or eligible assets.

Understand what has changed for the 2026 tax year

For property investors, the most important tax document this EOFY is the ATO’s 2026 rental property guide.

The guide sets out what investors need to know when preparing their 2025-26 tax return, including the rules around claiming rental expenses, interest deductions, repairs and maintenance, capital works, depreciation, record keeping, and apportionment where a property is used privately or rented below market value.

This matters because the ATO continues to closely monitor rental property claims, particularly interest expenses, repairs versus improvements, and deductions that are not properly supported by records. Investors should make sure their claims align with the 2026 guide and that they have the evidence needed before lodging their return.

While proposed tax changes announced in the May 2026 Federal Budget may affect future investment decisions from 1 July 2027, the immediate priority is getting the June 2026 EOFY position right. For investors, the practical message is simple: focus on compliance now, keep clear records, understand what can and cannot be claimed, and speak with a qualified tax adviser before lodging.

Think carefully before prepaying interest

Some investors consider prepaying up to 12 months of investment loan interest before June 30 to bring forward a deduction. This may be useful for some high-income investors, particularly where their taxable income is expected to fall next financial year.

However, it is not a strategy for everyone. It affects cash flow, may not suit every loan product and should only be considered with professional advice.

SP insight: Tax savings should never be the only reason to make a financial decision. The right structure must support your wider investment plan.

Plan for CGT before you sell

If you sold an investment property during FY26, remember that capital gains tax generally relates to the contract date, not settlement date. You should also confirm whether you held the property for at least 12 months and whether any capital losses can be applied.

With proposed CGT changes on the horizon, investors should also keep accurate purchase records, improvement invoices and valuation-related documents. These records may become even more important over the next few years.

Final word

EOFY is not just about lodging a tax return. It is an opportunity to sharpen your investment strategy.

For first-time investors, it is a chance to build good habits early. For existing investors, it is a moment to review performance and cash flow. For rentvestors and buyers considering another acquisition in FY27, it is a timely reminder that tax settings, lending conditions and asset selection all need to work together.

The best investors do not chase deductions for their own sake. They use EOFY to make better decisions, reduce avoidable risk and position their portfolio for long-term growth.