‘Rentvesting’ is a relatively new term that is being used to describe the action of buying property in an affordable area, renting it out to pay the mortgage, while then renting in an area that you would like to actually live in, or that makes more financial sense. Identified as the “most common new buying habit” in LJ Hooker’s The (new) Australian Dream white paper last year, Google Trends have also shown that the term has tripled in search requests.

There are a couple of types of rentvestors. Young people utilising the strategy and saving for a first home and an increasing number of professionally employed people of any age taking advantage of tax breaks and creating wealth through property investment rather than ownership.

Tommy Lim also comments rentvesting allows numerous clients to remain ‘globally mobile’ – either pursuing valuable work experience or further studies in overseas markets such Hong Kong, London or in the United States.

Download Our Rentvesting eBookRenting gives the flexibility not to be locked into an owner occupied mortgage. You are free to travel and move around or upsize should the family grow at any time.

Rentvesting may be less financially straining by investing in a cheaper market, and gaining access to the various tax concessions currently available.

Many first homes are not ‘dream’ homes and are often located where one can afford and further from work, amenities, family and friends. Also to fit a budget, various other features such as number of bedrooms, car spaces, bathrooms may be sacrificed.

Instead of saving and saving to afford where one wants to live, they may be able to continue renting and enter a market elsewhere straight away. History shows that well selected property can quickly outperform average saving abilities.

The desired suburb to live may not contain the 15 Key Investment Drivers (explained later) and therefore the performance of the property may not produce the equity gain needed if the owner is looking to upsize in the future.

In today’s interest and tax environment, there are many investment properties that will produce a positively geared cash flow that may be used to supplement personal rental expenses.

If you are renting and not investing, then your rent money is not working for you in any way. Investing in a property and receiving rent from a tenant will offset this ‘dead’ rent money and also provide some capital appreciation.

If the landlord decides to sell then you may be forced to move.

As you don’t own the property it may be harder to alter the dwelling to your taste or requirements.

Currently if you sell an investment property there will be capital gains tax to pay on any profit (a 50% discount may apply on property held longer than 12 months). Owner occupied homes are exempt from any capital gains tax.

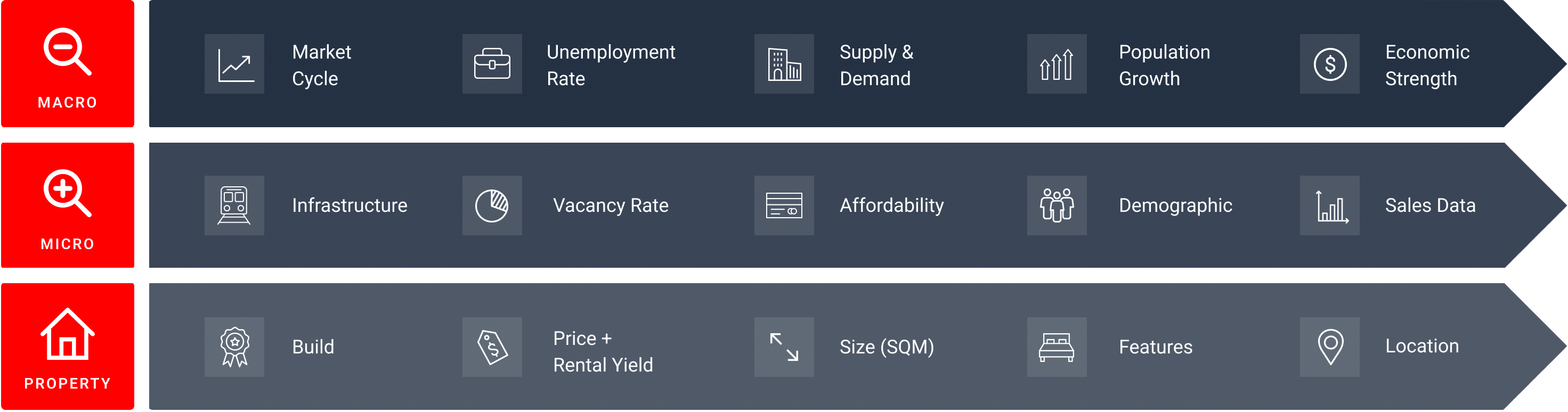

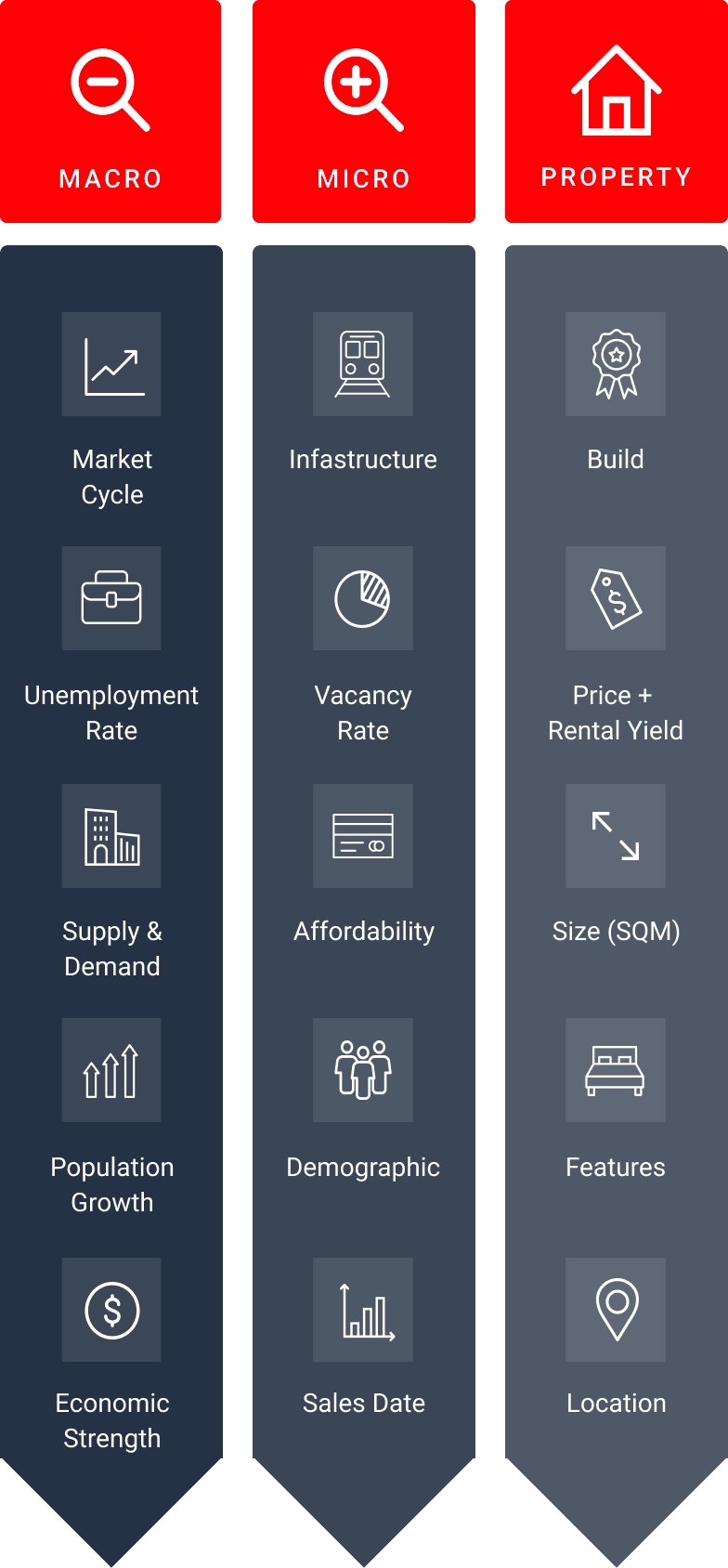

At Sound Property we use 15 Key Investment Drivers as a preliminary guide

Landbank with future subdivision potential

Huge block of land with the ability to subdivide into two well-sized building blocks.

Diversify NSW + QLD portfolio with a low maintenance investment

A proven performing suburb with a long-term growth rate of 8.36% p.a

Affordable investment property with high yield to help offset mortgage repayments

Great result for a client that's used the strategy of 'equity in their home for investment'. A property so clean there were no items to be rectified after the building and pest inspection!

Landbank opportunity with development potential in future

Rare and affordable 3-lot infill subdivision only 20km to Brisbane CBD.

Inner city house for investment and relocation

Recently renovated and super convenient location

A SMSF requiring a renovated low-maintenance set and forget property.

Highly desirable area, family friendly, low vacancy rates with lots of competition for potential tenants, higher yielding area, low maintenance property perfect for a SMSF.

6 Middlemiss St, Milsons Point

Try our Cashflow Calculator, specifically developed for property investors.

Use the calculatorGet educated and make informed investment decisions on topics such as cashflow, due diligence, market assessment and more.

Learn MoreHave one of our Property Advisors call you to discuss getting started.